REPORT: Trade Wars, Market Turmoil: Australia’s Digital Opportunity

- Publisher : Venture Insights

- Publish Date : March 19, 2025

Abstract: The OECD has downgraded global GDP growth due to escalating trade tensions, primarily driven by U.S. tariffs on China, Canada, and Mexico. Financial markets have sharply declined, while the risk of a U.S. recession continues to rise. The real threat is its dependence on U.S. tech giants, which imposes substantial economic costs outside traditional trade figures (see our report “The tariff debate ignores Australia’s digital dependence”).

Australia will not escape the effects of the economic slowdown. What makes us see this as an opportunity? Australia’s low trade exposure to the U.S. market gives it freedom to respond that other countries lack. With global uncertainty growing, Australia has the opportunity to adopt a more strategic trade and technology policy to safeguard its economic future.

Trade turbulence hits growth forecasts

The OECD has downgraded global GDP growth as escalating trade tensions—driven primarily by U.S. tariff hikes on China, Canada, and Mexico—threaten to disrupt global supply chains. With the U.S. doubling down on its “America First” economic stance, key trading partners are formulating counterstrategies, increasing the risk of a prolonged economic standoff.

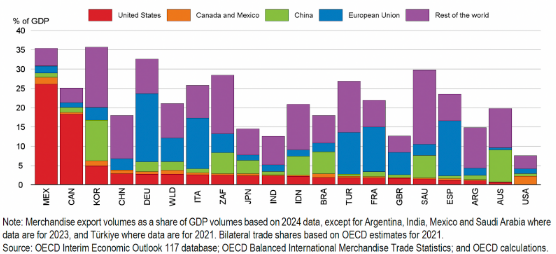

Figure 1: 2024 distribution of merchandise export volumes (% of GDP)

Stock markets have reflected this growing uncertainty, with sharp corrections across global indices as investors brace for slower growth and potential policy missteps. The likelihood of a U.S. recession is gaining traction, with monetary policy constraints limiting the Fed’s ability to cushion the downturn, especially as inflationary pressures persist.

OECD Economic Outlook – Key Takeaways (March 2025)

- Global Growth Slows Amid Rising Uncertainty

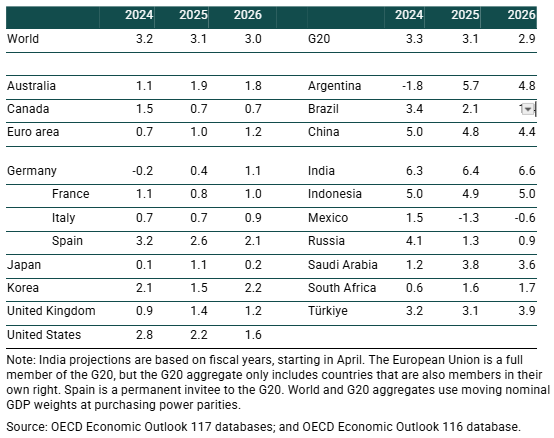

Global GDP growth is projected to moderate from 3.2% in 2024 to 3.0% in 2026, with advanced economies experiencing slower expansion due to weaker investment and household spending. The U.S., Eurozone, and China face downward pressure from heightened geopolitical risks and trade tensions. - Inflation Eases but Remains Above Target

While headline inflation in G20 economies is expected to decline to 3.2% by 2026, core inflation remains sticky in several countries. Rising trade costs and persistent wage pressures could delay monetary policy easing. - Trade Barriers Threaten Economic Stability

Tariff increases, particularly between the U.S., China, Canada, and Mexico, are expected to weigh on global trade and push up inflation. Further fragmentation of the global economy could shave 0.3% off global GDP in the next three years. - Financial Markets Face Growing Volatility

A sharper-than-expected slowdown could trigger asset repricing and financial instability, particularly in equity and debt markets. Rising interest rates in some economies and geopolitical tensions add to investor uncertainty. - Policy Action Needed to Ensure Stability

Central banks must balance inflation control with economic growth, while fiscal discipline is crucial to ensure debt sustainability amid rising spending pressures. Governments should focus on bilateral trade cooperation, regulatory reforms, and AI-driven productivity enhancements to sustain long-term growth.

Who are the biggest losers from a trade war?

The OECD simulation highlights that a 10% tariff increase by the U.S. and reciprocal tariffs from other countries would be a major self-inflicted blow to the U.S. economy. As shown in the chart, the U.S. would face a GDP decline of around 0.8% by year three, with Mexico (-1.2%) and Canada (-0.7%) also among the biggest losers due to their deep trade ties with the U.S. This policy mainly harms America’s own economy and its closest trading partners, while the global impact is milder.

Figure 2: OECD modelling of tariff-related GDP impacts

Why is the U.S. Targeting China, Mexico, and Canada?

The U.S. has imposed higher tariffs on China, Mexico, and Canada due to their significant roles in its trade ecosystem and ongoing economic and geopolitical concerns. These three countries collectively account for over 40% of total U.S. trade, making them pivotal in both supply chains and domestic economic policy:

- China – A Geopolitical and Economic Rival

The U.S. sees China as its primary competitor in global trade and technology, leading to ongoing tensions over industrial policy, intellectual property, and trade imbalances. The 20 percentage point tariff increase on Chinese goods aims to reduce dependence on Chinese imports and counter what the U.S. views as unfair trade practices and industrial subsidies. - Mexico & Canada – North American Trade Dynamics

As the U.S.’s top two trading partners, Mexico and Canada are deeply integrated into U.S. supply chains under the USMCA. The new 25 percentage point tariff hike on their merchandise exports is likely aimed at renegotiating trade terms, reshoring manufacturing, and addressing concerns over trade imbalances and rules of origin compliance. - Steel, Aluminium, and Energy – Protecting U.S. Industry

The U.S. has long sought to protect its domestic steel and aluminium industries from global oversupply, particularly from Canada, which is a major exporter. The tariffs on energy products and potash suggest a broader push to strengthen U.S. energy security and reduce reliance on key raw materials of its neighbours. - Strategic Leverage for Trade Negotiations

By imposing tariffs, the U.S. gains bargaining power ahead of potential trade renegotiations. The timing aligns with upcoming U.S. policy reviews and a mid-term election year, where protectionist policies often gain political traction.

Overall, these tariffs reflect both economic and political calculations, aiming to reshape supply chains, support domestic industries, and reinforce U.S. strategic interests in global trade.

Australia’s response

Importantly, Australia has a relatively low exposure to the U.S. market. Our merchandise trade is small, and services trade is also highly unbalanced in favour of the U.S.. This highlights the gratuitousness of the U.S. move to impose tariffs on Australia exports. But it also gives Australia a degree of freedom in its response to U.S. aggression that countries like China, Canada, and Mexico lack.

For Australia, the real challenge goes beyond merchandise trade disputes – its economic vulnerability lies in its dependence on U.S.-based digital platform giants. The full costs of this dependence are not captured in traditional trade figures. Treasurer Jim Chalmers has warned of a multibillion-dollar dent in Australia’s economy by 2030 due to rising trade tensions, reinforcing the urgency for a more deliberate, sovereign approach to global economic shifts. The current disruption brings an opportunity to rewrite Australia’s relationship with U.S.-based digital platforms.

With a weaker budget outlook and a turbulent global economy, Australia must redefine its trade and tech strategy, balancing economic resilience with geopolitical realities. The message for Canberra is clear: the world is rewriting the rules of economic engagement, and Australia must adapt – or risk falling behind. This means:

- Adjusting regulatory and tax treatment of U.S.-based digital platforms to combat their extractive practices.

- Bolstering sovereign technological, cultural, economic and military capabilities.

- A more transactional approach to sharing those capabilities.

Venture Insights will be developing potential scenarios and options for such a strategy in the coming weeks.

Figure 3: Five Key Implications for Australia’s TMT Sector

Source: Venture Insights

Appendix

OECD Global GDP Outlook

OECD Global Inflation Projections

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.