REPORT: ANZ FWA growth challenges NBN and UFB

- Publisher : Venture Insights

- Publish Date : April 11, 2025

Abstract: Australia’s NBN and New Zealand’s UFB providers face rising competition from various sources, including competitive fibre, LEO satellites, and MNO fixed wireless providers. In Australia FWA growth is picking up, continuing to pressure NBN. A 10% FWA share of broadband by FY28 remains plausible.

In the more mature New Zealand market, penetration is higher at around 20% of the broadband market. Spark data shows that its FWA growth now approximates population growth. However, One NZ and 2degrees’ relatively low share of FWA connections suggest there may be more growth available.

The rise of FWA threatens NBN and Chorus with subscriber losses, pricing pressure, and potential asset underutilisation, particularly in price-sensitive or urban markets. However, their fixed-line networks offer unmatched reliability and capacity, creating opportunities to target premium customers, support FWA backhaul, and drive economic benefits. By adapting pricing, accelerating fibre, and exploring partnerships, both operators can mitigate risks and carve out a complementary role alongside FWA in Australia and New Zealand’s broadband markets.

ANZ FWA growth challenges NBN and UFB

Abstract: Australia’s NBN and New Zealand’s UFB providers face rising competition from various sources, including competitive fibre, LEO satellites, and MNO fixed wireless providers. In Australia FWA growth is picking up, continuing to pressure NBN. A 10% FWA share of broadband by FY28 remains plausible.

In the more mature New Zealand market, penetration is higher at around 20% of the broadband market. Spark data shows that its FWA growth now approximates population growth. However, One NZ and 2degrees’ relatively low share of FWA connections suggest there may be more growth available.

The rise of FWA threatens NBN and Chorus with subscriber losses, pricing pressure, and potential asset underutilisation, particularly in price-sensitive or urban markets. However, their fixed-line networks offer unmatched reliability and capacity, creating opportunities to target premium customers, support FWA backhaul, and drive economic benefits. By adapting pricing, accelerating fibre, and exploring partnerships, both operators can mitigate risks and carve out a complementary role alongside FWA in Australia and New Zealand’s broadband markets.

FWA pricing gap driving takeup?

In Australia, 2023 and 2024 NBN wholesale price changes saw Basic and Standard tier prices rise, while Superfast and Ultrafast NBN prices have fallen. In contrast, FWA prices have remained relatively stable over the same period, widening the price gap between FWA plans and equivalent low-end NBN plans. This has increased the appeal of FWA plans and has provided an opportunity for FWA providers to grow their subscribers.

There has been significant and growing discounting on NBN retail plans since September last year (see our report “Australian NBN discounting drives challenger growth”). But these are mostly focussed on high end plans. And some retailers have added discounts on FWA plans too, maintaining their relative appeal.

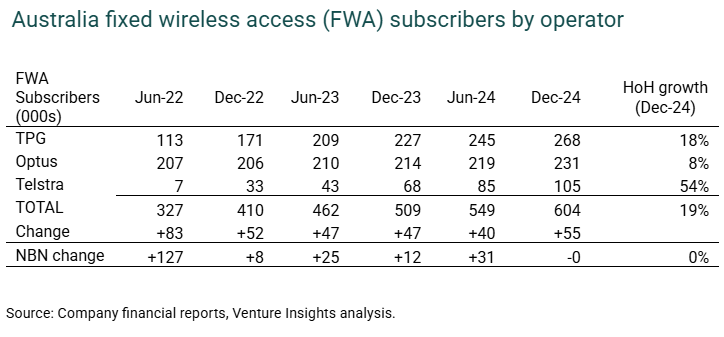

As we noted last September (see our report “Fixed wireless keeps up the pressure on fixed broadband”), the number of wireless broadband (FWA) subscribers in Australia has been growing, but that growth was slowing in 2023. Telstra had been building momentum in this space, TPG was still growing but more slowly, and Optus relatively is stable.

Since then, all three of Australia’s MNOs reported accelerated growth in FWA subscribers during the December 2024 half. Overall June 2024 FWA growth of +40k services was slightly lower than December 2023 (+47k). But while the overall volume was only slightly down in that half, the three operators saw different results. TPG saw the strongest growth, adding +18k FWA subscribers, while Telstra followed closely at +17k. Optus FWA saw minimal growth, adding just +5k services, similar to the prior half.

The most recent data shows an elevated level of overall growth, but shared out similarly amongst the three operators. Last year we suggested that growth might pick up as the price gap between FWA and NBN began to bite, and that seems to be happening.

Optus’ FWA performance up to now has been sluggish, despite Telstra and TPG clearly showing that there is customer appetite for FWA. In the June-24 quarter, Optus introduced more aggressive promotional offers on its 5G Home Internet plans. These plans are already $15-$20pm cheaper than Optus’ corresponding NBN plans and we observed Optus offering an additional $10-$20pm off for the first six months, on top of its existing offer of ‘first month free’. This now appears to be driving some new growth for Optus, with +12k added in December 2024. This is their biggest jump in years.

Overall, growth in the December 2024 half was 55K, up significantly from the 40K in the previous June half. However, the change is small in absolute terms. Overall, we see a linear growth trend which we expect to persist for several more years, bringing total MNO FWA numbers up towards 900k by FY28.

The contrast with New Zealand is instructive. There is much less data available in the New Zealand market, but ComCom data shows that there were 378k FWA connections. This accounted for 20% of the broadband connection share in June 2023, the latest year for which data is available.

Spark results show that park is the biggest FWA provider, with 209k of those connections. However, growth since then has been low, reaching only 218k in December 2024. This growth approximates population growth, suggesting that Spark’s FWA business is maturing.

But this does not rule out further growth from One NZ and 2degrees. In fact, these are underweight on FWA compared to Spark, and we expect them to drive further gains over the coming years, lifting overall penetration beyond 20%.

Threat to NBN and UFB

As we have noted before, NBN, Chorus and other UFB operators face rising competition from several sources. FWA in particular is adding to competitive pressure and has financial consequences for wholesale operators:

Increased Competition and Subscriber Churn

FWA, particularly 5G-based solutions offered by mobile network operators, provides an alternative to fixed-line broadband. With FWA offering higher speeds (often exceeding 100 Mbps), customers may switch away from NBN or Chorus services. In Australia, NBN has faced net churn due to competition from 4G/5G FWA, as mobile operators roll out affordable plans. NBN is particularly vulnerable in FTTN areas, and has launched its fibre upgrade program at least partially in response to wireless alternatives. This churn erodes the subscriber base, spreading fixed infrastructure costs over fewer customers, which could strain financial sustainability.

In particular, FWA tends to appeal to price-sensitive customers or those on lower-speed plans (e.g., 25–50 Mbps), as it delivers comparable performance at potentially lower costs. This could hollow out demand for NBN and Chorus’s entry-level wholesale products. FWA’s rise could shift their customers to mobile-based providers, reducing overall wholesale demand.

NBN’s multi-technology mix (FTTP, FTTN, HFC, fixed wireless, satellite) makes it vulnerable to FWA in urban areas, where 5G is rapidly expanding. However, its mandate to serve all Australians, including remote regions, ensures a baseline demand for fixed wireless and satellite services where FWA isn’t viable. NBN’s challenge is balancing urban price competition with rural cross-subsidies, as FWA could exacerbate pricing tensions.

Pressure on Pricing and Margins

FWA’s lower deployment costs allow mobile operators to offer competitive retail prices. This puts downward pressure on wholesale prices that NBN and Chorus can charge retail service providers (RSPs). Chorus, with its focus on fibre, may face pressure to reduce wholesale prices for high-speed plans to compete with FWA’s value proposition.

Risk of Stranded Assets

Both NBN and Chorus have invested heavily in fixed-line infrastructure (fibre for Chorus, a mix of fibre, FTTN, and HFC for NBN). Higher FWA adoption could underutilise these assets, with obvious financial impacts. In Australia, NBN’s fixed wireless and satellite services already serve regional areas, but urban FWA growth could reduce demand for fixed-line upgrades, leaving costly infrastructure underutilised. Similarly, Chorus’s fibre-to-the-premises (FTTP) rollout could see lower uptake if FWA gains traction in urban centres.

Opportunities for NBN and Chorus

The news is not all grim. FWA’s strengths – quick deployment and flexibility – come with limitations, such as spectrum constraints and variable performance during peak usage. NBN and Chorus can position their fixed-line networks as reliable, high-capacity backbones for hybrid solutions. For instance, NBN’s fixed wireless upgrades (e.g., Home Fast and Superfast plans reaching 500 Mbps) show potential to compete with FWA in regional areas, while Chorus’s fibre offers unmatched reliability for businesses and high-bandwidth applications. By partnering with RSPs to bundle fixed and wireless services, both operators could retain relevance.

Focus on Premium and Business Markets

FWA may capture a share of the mass market, but NBN and Chorus retain an advantage in premium residential and enterprise segments with fibre’s superior speeds (up to 1–8 Gbps) and low latency. In New Zealand, Chorus’s Hyperfibre plans have seen price reductions to attract high-value customers, countering FWA’s appeal. NBN’s fibre upgrade program, aiming to expand FTTP coverage, could similarly cater to users needing consistent performance for gaming, streaming, or remote work, where FWA may struggle under congestion.

Leveraging Infrastructure for Backhaul

Both NBN and UFB operators have explored using their extensive fibre networks for backhaul for FWA towers. As mobile operators expand 5G FWA, they’ll need robust backhaul to handle increased data traffic. NBN and UFB providers could monetise this by leasing fibre capacity to mobile carriers, offsetting losses from retail churn.

Service Innovation

To counter FWA, NBN and Chorus could enhance wholesale products with value-added services, such as guaranteed speeds, low-latency tiers for gaming, or bundled cybersecurity features. NBN’s recent removal of capacity-based charging for higher-speed plans has improved RSP flexibility, enabling better retail offerings. Chorus could similarly innovate by offering dynamic bandwidth allocation or tailored enterprise solutions, maintaining wholesale demand despite FWA growth.

In summary, NBN and UFB strategies are to:

- Accelerate Fibre Upgrades: Prioritise FTTP to offer superior performance, reducing churn to FWA.

- Optimize Pricing: Simplifying wholesale pricing to help RSPs compete with FWA’s cost advantage. The elimination of capacity ricing in Australia will help with this.

- Collaborate with Mobile Operators: Explore backhaul partnerships or hybrid offerings to share infrastructure benefits.

- Enhance Customer Experience: Focus on reliability and value-added services to differentiate from FWA’s variability.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.