BRIEF: Inflation linked pricing is a delicate balancing act

- Publisher : Venture Insights

- Publish Date : June 30, 2023

Inflation linked pricing is a delicate balancing act

TLDR version: The latest monthly inflation data shows the gap between communications prices and the general level of prices continues to widen. Telcos in Australia and abroad have in recent years introduced price rises linked to the level of inflation. This is now producing a backlash in the UK, with double-digit price hikes attracting attention from politicians and regulators.

Inflation based pricing remains a valid option for Australian telcos seeking revenue growth. Our lower inflation levels (vs UK) should make the magnitude of the increases more palatable. However pricing and public relations will need to work closely to ensure the public and politicians understand the necessity of any price increases.

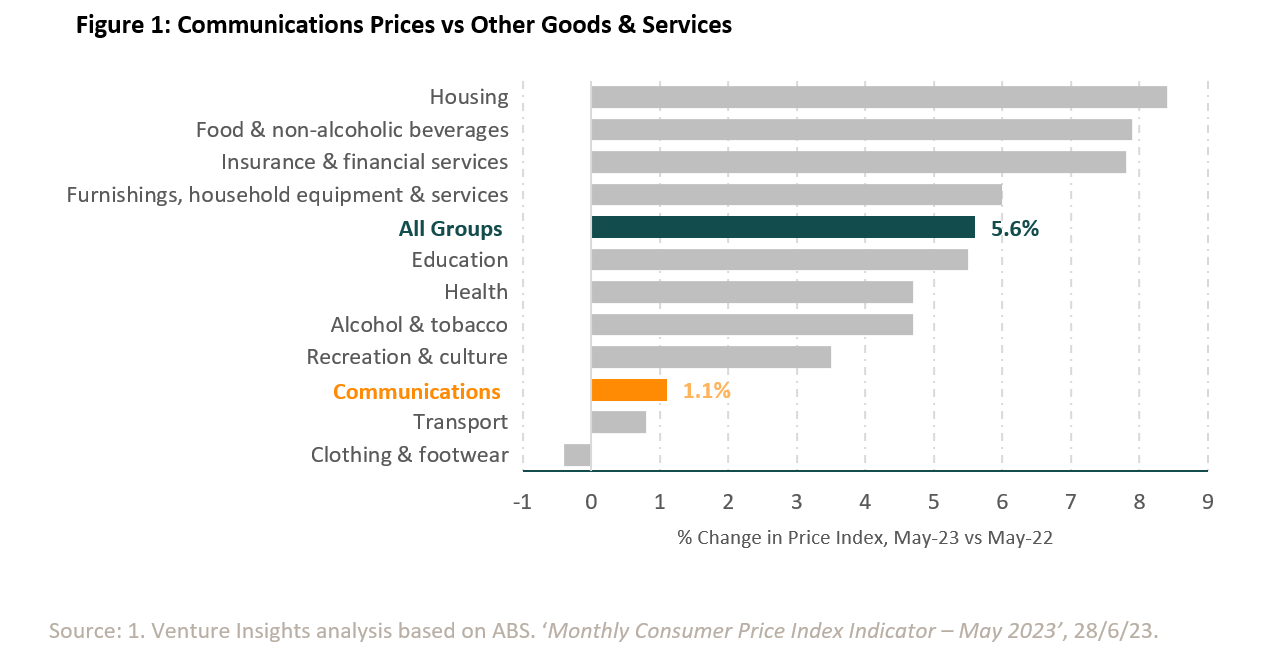

Communications pricing continues to rise at a slower rate than CPI.

This week, the Australia Bureau of Statistics (ABS) released its latest monthly consumer price indicator covering the period up to May 2023. At a macro level, the data shows the inflation rate has resumed its downward track. The Consumer Price Index (CPI) rose 5.6% during the twelve months to May 2023. This is down from 6.8% reported last month and compares favourably to the peak of 8.4% recorded for the twelve months to December 2022.

The ‘Communications’ category of the CPI continues to see price rises well below the general inflation rate. Communications prices rose +1.1% for the twelve months to May, vs 5.6% for the overall level of consumer prices.

As highlighted in our recent ‘State of the Telecommunications Industry’ report, during the period between June 2012 and March 2023, the price of ‘Telecommunications Hardware and Services’ fell by 24.6%, versus a rise in the overall CPI of over 32.6%. The latest data suggests the gap between telecoms prices and overall consumer prices is continuing to grow. This is despite major telcos having introduced inflation linked prices rises over the last year, and flagging the potential for further increases this year.

The backlash to inflation linked pricing in the UK

UK telcos began introducing inflation linked pricing earlier than their Australian counterparts. BT has had annual price rises for a number of years, but in September 2020 it introduced a new policy across its consumer portfolio of annual prices rises equal to CPI + 3.9%. Several other UK telcos have followed suit, also introducing annual price rises based on a CPI+ basis.

While inflation remained low, these price rises produced consumer grumblings but appeared to be tolerated. With double digit inflation in the UK, patience with this approach may be wearing thin. The practice has drawn the attention of politicians, with the Chancellor of the Exchequer to meet industry regulators including Ofcom and the ‘Competition and Markets Authority’. Expected to be on the agenda is not only the overall magnitude of the price rises, but also the fact BT, Vodafone and Virgin Media are all adding the same +3.9% on top of their chosen inflation measure (and TalkTalk a very similar 3.7%).

Why does this matter?

In the near term, Australian telcos are expected to see their revenue growth aided by rising immigration. But volume growth is only part of the equation. The sector also needs to see improved ARPU to offset rising costs for labour and capital. Cost cutting and productivity gains can arguably only carry the industry so far. Upselling customers may also become more difficult if cost of living pressures remain or the economy experiences a significant downturn.

Inflation linked price rises applied to existing customers are an opportunity to grow ARPU at a higher rate than targeting new customers alone. As the UK experience shows however, a ‘CPI plus’ approach while good for revenue, has the potential to spark a backlash

In the Australian context, we believe there remains a rationale for operators to introduce inflation linked price rises. Price rises accompanied by increases in plan inclusions, a ‘more for more’ approach, may help mitigate the risk of a UK style backlash. It will also be necessary to bring policy makers and customers on this journey, so they understand why they are being asked to take on this extra burden. The next round of prices increases, if telcos go through with them, will therefore very much need to be a joint mission shared between pricing and public relations teams.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to www.ventureinsights.com.au or contact us at contact@ventureinsights.com.au