BRIEF: ARN Media investment shows long-term confidence in radio

- Publisher : Venture Insights

- Publish Date : June 21, 2023

BRIEF: ARN Media investment shows long-term confidence in radio

TLDR version: ARN Media’s stake in Southern Cross Austereo (SCA) might not seem to make much sense. The SCA share price has declined over the last twelve months while some other media stocks have risen, and radio ad revenue has been slow to recover from the pandemic. But there is considerable upside in radio in the medium to long term because it is only just beginning its transition to online delivery. ARN Media’s stake is a bet on this long-term future.

ARN Media’s investment is a bet on online audio’s potential

Southern Cross Austereo (SCA) is a business dominated by radio, and to a lesser extent regional TV. This has weighed on the company as radio has been relatively slow to recover from the pandemic. Regional Australia has also been relatively slow to recover from the pandemic. In contrast, metro FTA TV has boomed over the last eighteen months (though a slowdown is now happening).

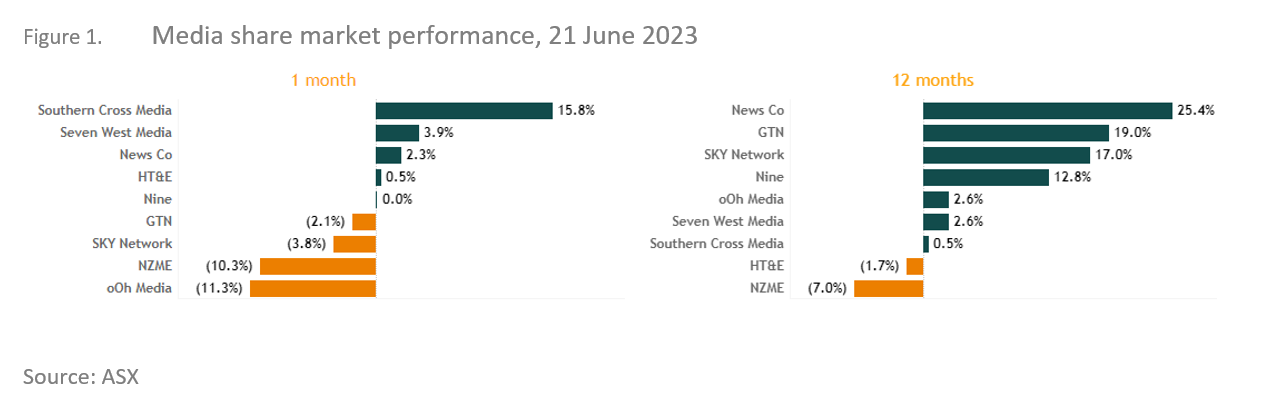

As a result, SCA has underperformed other media stocks. After a bad June 2022 (when all media stocks fell) SCA and ARN Media (formerly HT&E) have basically held their ground while most other media stocks have recovered. Incidentally, SCA’s “holding ground” includes the roughly 15% bounce that SCA shares received this week after ARN Media’s purchase – it was down before that.

ARN Media owns 58 radio stations across 33 markets plus 46 DAB+ stations nationwide, with key brands including KIIS, Mix and Gold FM. In addition it operates the digital entertainment platform, iHeartRadio. SCA owns 99 radio stations under the Triple M and Hit network brands across FM, AM, and DAB+. SCA also operates its LiSTNR app, housing radio, podcasts, music, and news. In addition it broadcasts TV in most Eastern and Central regional TV markets, including Tasmania, Darwin, Broken Hill, and Spencer Gulf.

This week, ARN Media boosted its stake in SCA to 14.8%, the maximum allowed under cross-media laws, in a strong vote of confidence in the company.

This may be the first step in a plan to merge the companies (requiring regulator approval) or it may be a financial investment like ARN Media’s 2021 investment in oOH!media which netted it a tidy profit when the outdoor advertiser’s valuation later surged.

From the perspective in industry performance, it doesn’t matter. The investment is a demonstration of confidence in the radio sector. But given past performance, why this confidence?

Our view is that the radio industry has significant upside to come in digital audio. We estimate that only 3% of radio industry revenues currently come from online platforms. The penetration of radio industry apps was 36% in our 2022 consumer survey (2023 update coming shortly), a good performance with plenty of headroom for growth. But the business models take longer to develop, so revenue growth lags penetration.

The contrast to television is instructive. We estimate that around 12% of FTA TV advertising revenue is now from its BVOD platforms. Importantly, BVOD yields ($ per minute of viewing) are significantly higher than broadcast yields, and while both rose in FY22 the gap also widened. So while FTA viewing is falling fast, revenue has been much less impacted as continued migration to BVOD is putting FTA TV is a strong position structurally.

We estimate that radio is around four years behind the FTA TV sector in its digital transition. If that is correct, then radio should expect significant digital revenue uplift over the next few years.

Why does this matter?

The ongoing viability of FTA television and radio is imperative in Australia. Our unique geography and population distribution makes broadcast service delivery a lifeline and safety net for many communities, not least the roughly 15% of premises that have no fixed broadband connection at all. The efficiency and reliability of broadcast communications in times of emergency gives it a social role that telecommunications networks find hard to replicate.

Rising competition in video and audio service markets has placed a question mark over the long-term viability of traditional broadcasting. FTA TV viewing is falling. While radio listening is more robust, competition from global streaming and podcast providers is piling up. This is an issue for both industry and government.

For industry, it is a threat to industry finances and as a result to the maintenance of broadcast transmission infrastructure.

For the Federal Government, it is a threat to the delivery of broadcast services that remain in high demand and support policy objectives in the social and cultural spheres. The commitment of the Government to these objectives should not be underestimated; only this week, the Minister for Communications responded to the ABC’s “online first” philosophy with a sharp reminder that the ‘B’ in ABC stands for broadcasting, and that this cannot be neglected.

Our view has always been that online TV and audio will not replace traditional broadcasting but complement it. The result will be the emergence of a hybrid broadcast/online model of FTA media delivery that will exploit the best features of both platforms and increase opportunities for cross-promotion.

Clearly, there is much at stake in the success of this hybrid model, which is needed to underpin a viable FTA industry. ARN Media’s investment is a clear vote of confidence in the future of this model.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe, with a special focus on new disruptive technologies.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.