BRIEF: 2023 Data centre outlook and forecast released

- Publisher : Venture Insights

- Publish Date : April 11, 2023

2023 Data centre outlook and forecast released

TLDR version: Venture Insights has published its 2023 Australia Data Centre Forecast & Outlook. We predict that AU datacentre capacity will grow at CAGR 24.5% to reach 2.8MW in FY27. Revenues will grow more slowly at CAGR 18.5% to reach $4.2bn in FY27 as price per MW falls. Sydney’s dominance will strengthen despite growth in Melbourne, Perth, and Brisbane, as Microsoft, AWS and others expand their datacentre investments in the Emerald City.

Data centre set for long-term growth

The Australian data centre (DC) market is expanding, forecast to rise from $1.8bn to over A$4.2b by FY27. Volume will rise from 894MW in FY22 to nearly 2.8 GW by the end of FY27. The major providers of DC capacity in Australia are a mix of international players and Australian based DC specialists. We predict some reshuffling of leadership compared to FY20, with AirTrunk and particularly NextDC coming to the fore.

Currently, the majority of data stored in outsourced DCs is from enterprise and government clients. However, the market is moving towards the hyperscale segment with the ongoing shift to cloud-based computing. We predict hyperscale will generate 39% of total DC revenue by end FY27, and 59% of total supply by then if internal hyperscale capacity (which generates no DC revenue) is included. Telcos, who once hoped to dominate the industry, still have a presence but are now marginal.

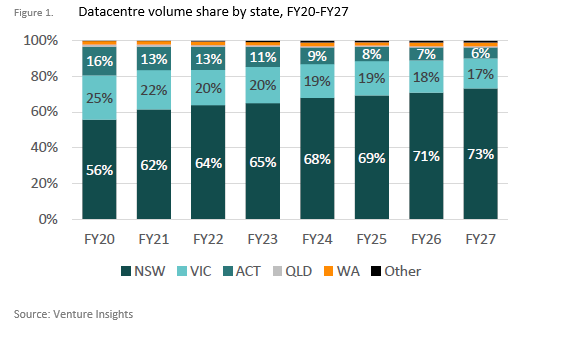

New data centres and expansions have been announced in peripheral markets, including some small edge facilities in regional Australia, and larger centres in areas where submarine cables have made landfall such as Perth, Darwin and Brisbane. But the majority of investment is headed to Sydney which is the centre of hyperscale activity, entrenching Sydney’s dominance of the DC market.

Why does this matter?

Along with telecommunications networks, DCs are a workhorse of the national digital economy. The long-term growth we forecast for the industry reflects the growing ‘cloudification’ of business and household life over the coming years, with higher workloads arising from cloud-based enterprise apps and video entertainment (including VR).

The industry is broadly doing well and is highly attractive to investors who are looking for good, reliable growth prospects.

Despite the industry’s success, many major players are privately held and rely on debt and cashflow to fund expansion. AirTrunk and Canberra Data Centres stand out, but new privately held operators are also emerging in the peripheral markets. If capital markets settle over the next few years, we expect to see sale activity tick up as existing owners seek to cash in on the industry’s investment profile.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to www.ventureinsights.com.au or contact us at contact@ventureinsights.com.au