BRIEF: TPG network sharing deal is lifting mobile competition

- Publisher : Venture Insights

- Publish Date : March 6, 2025

Abstract: TPG’s full year results announcement was accompanied by remarks on the emerging impact of TPG’s recently activated network sharing deal with Optus. TPG reported significant boosts in prepaid and postpaid signups on the strength of its expanded network coverage and depth. We expect Telstra to be most affected by TPG’s new strength.

TPG highlights potential for regional mobile growth

During TPG’s annual results briefing for the year ending December 2024, Berroeta highlighted the outcomes achieved within the first month of its network sharing agreement with Optus. The deal with Optus is a significant development for regional customers and TPG itself, as well improving overall economic returns on regional mobile infrastructure.

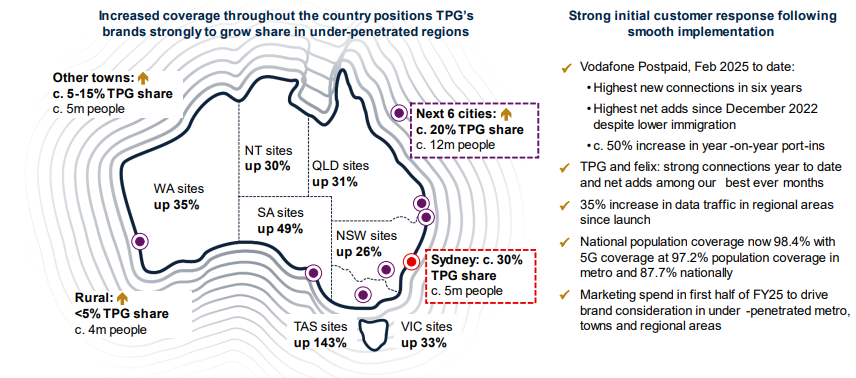

Berroeta emphasised the impact of expanding Vodafone’s geographic reach. He noted that within just a week of activation, regional data traffic in Victoria nearly doubled. Berroeta expressed optimism about TPG’s potential to increase its national market share to match levels seen in Sydney (around 30%).

Since the launch of regional network sharing, TPG has recorded its highest postpaid connections in six years and its highest postpaid net additions in over two years. Additionally, there has been a 50% year-on-year increase in customer wins from competitors. Berroeta also mentioned that both TPG and Felix Mobile sub-brands are also experiencing strong sales, with regional data traffic increasing by 35%.

Figure 1: TPG 2025 mobile performance to date

Source: TPG 2024 financial results

Mobile discounting driving competition

The mobile market has seen ARPU increase over the last year or so, but remains competitive, with significant discounting in high-end postpaid plans and for median prepaid plans, coupled aggressive handset discounting

There have been mixed results. Reviewing reported results to December, Optus and Telstra both saw around 1% postpaid connection growth, basically the rate of population growth. In prepaid, Optus outran Telstra, growing 2.9% to Telstra’s 0.6% pcp.

TPG was behind its competitors in postpaid, with connections falling 1.7% in the December half pcp. However, it outstripped both Telstra and Optus, growing connections by 4.2% over the course of the year.

Why does this matter?

So what does TPG/Vodafone’s rising appeal mean for mobile competition?

First, we expect wider differentiation between TPG’s various mobile brands, widening its addressable market. Stronger coverage gives Vodafone the opportunity to position itself as a more premium brand. This will differentiate Vodafone more from other TPG brands such as Lebara and Felix, increasing its appeal in the postpaid market where Telstra has the most to lose.

Second, also we expect TPG’s non-premium brands to benefit as well, which will lift competition in prepaid. Telstra’s relative weakness in prepaid makes it a target for TPG customer wins, and we expect some rejigging of Telstra’s prepaid offer to manage the impact. Differentiation between TPG and Optus is now lower, so we also expect an effect on Optus’ prepaid momentum as well. Of course, Optus gains the lion’s share of TPG’s regional revenue through its wholesale arm, so the effect is more pronounced on Telstra than on Optus.

In summary, we think that Telstra bears the brunt of the impact over time. Optus has wholesale revenue to compensate for any retail losses. This, presumably, is the prediction that Optus made when it offered TPG a network-sharing deal. That prediction will probably be borne out, especially in a slow economy where households and businesses are looking for new low-cost alternatives. Optus’ March results will be the first opportunity to see how mobile competition is unfolding.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to www.ventureinsights.com.au or contact us at contact@ventureinsights.com.au