REPORT: Breaking the Consensus – future media scenarios

- Publisher : Venture Insights

- Publish Date : April 4, 2025

Abstract: Venture Insights has forecast media advertising outcomes for many years. Recent events suggest that greater uncertainty is coming, as the established Consensus about the post-Cold War period falls away (see our report “Breaking the Consensus – media futures in a fractured world”).

Responding to this reality, we have reviewed our base case assumptions for media, and have developed several alternative scenarios that reflect potential shifts in the media ecosystem. These include three scenarios that respectively incorporate heightened economic nationalism (“Fortress Australia”), social conservatism (“Social Backlash”), and technocratic libertarianism (“AI-powered”). This report outlines these scenarios, and will support quantitative forecasting of their implications in subsequent reports.

We invite you to get in touch if you’d like to explore what these scenarios mean for your specific segment of the media value chain – and how you can prepare to navigate what comes next.

Media markets after the Consensus

In the media industries, the collapse of the Consensus will force governments to review the fundamentals of the media policy framework. In a more nationalistic and competitive world, the dominance of globalised digital platforms is potentially problematic, but also more open to challenge. Consumers may withdraw from engagement with platforms perceived as unaligned with national or community interests. Governments may seek to curb their influence in favour of locally-accountable media.

The media market has already seen major change over the last decade. Media has been increasingly dominated by global digital platforms, and the growth of these platforms was a result of the Consensus. These platforms also reinforced the Consensus by globalising the sources of information and entertainment at the expense of local media.

But more recently, there are also indications of a shift in the media market. Major disruptors have already emerged.

AI at Breakneck Speed – Beyond Human Control: Artificial intelligence is no longer just an efficiency tool; it is a market-shaping force. The rapid acceleration of generative AI is creating media content, personalising advertising, and disrupting traditional revenue models at an unprecedented scale. Any hope of slowing AI adoption is wishful thinking – the genie is out of the bottle, and global players such as Google, Meta, and Amazon are doubling down on AI-driven advertising ecosystems that could bypass traditional media entirely.

Regulatory Backlash Against Big Tech: While the US pushes for unrestricted AI development, Australia and other nations are taking a different approach. Europe has already implemented sweeping digital regulations, and Canada, India, and Australia are considering tighter controls on global platforms that have drained local advertising dollars. The battle between platforms and regulators is intensifying – just as it did when Meta briefly blocked Australian news content in 2021. If Australia follows through with more aggressive policy intervention, local players like News Corp Australia, Nova Entertainment, and outdoor media giants like oOh!media stand to gain.

Consumer Disengagement from Social Media – The Tipping Point: The unchecked rise of social media may finally be hitting its limits. Consumer trust is at an all-time low, with misinformation, privacy breaches, and addictive design fuelling a backlash. Younger audiences are reducing time spent on legacy platforms like Facebook, while TikTok faces regulatory scrutiny. If audiences turn away from social platforms, advertisers will follow, leading to a reallocation of ad spend. Traditional media brands like Nine, Seven, and ARN Media could benefit – if they adapt in time.

Global Media Fragmentation – A Fractured Future: The dream of a single, borderless digital media market is fading. Protectionist policies, nationalistic sentiment, and local content regulations are splintering the global media landscape. Countries like China and India have already banned or heavily restricted foreign platforms, and similar discussions are emerging in Australia. If local governments take a stronger stance, Australian-owned platforms like Stan (Nine), Kayo (News Corp), and SBS On Demand could see a resurgence, while Google and Meta face fresh hurdles.

In Australia specifically, the growth trends of the last decade are increasingly exhausted:

- FTA TV recovery: Australian FTA Total TV viewing rose by 1.2% in calendar 2024, reversing a long term trend of annual declines due to the impact of SVOD viewing growth (VOZ 2024, Venture Insights 2025).

- SVOD flattening: In contrast to FTA TV, SVOD viewing in Australia appears to have fallen in 2024 (Deloitte, 2024).

- Social media engagement flattening: Social media participation in Australia rose by only 0.5% over 2024, after falling 3.5% in 2023, suggesting that social media engagement has peaked. (Kepios 2025)

- Digital advertising effectiveness concerns: The American Association of National Advertisers has estimated that less than half of digital ad spending actually reaches consumers, despite some recent improvements (ANA 2024).

The maturing of several media industries like SVOD and social media, plus rising pressure to demonstrate advertising effectiveness, challenges the dominant media trend of the last decade: galloping digital platform growth.

The market now seems to be taking a deep breath before a new phase opens up. New trends will take over, though it is difficult to predict exactly which trends. However, they will certainly be conditioned by the changes that occur in the wider economic and political environment, themselves highly uncertain.

Four Future Media Scenarios

As global dynamics shift and the digital economy matures, Australia’s media landscape stands at a crossroads. From the disruptive power of artificial intelligence to rising geopolitical tensions and growing public distrust in major platforms, the rules of engagement are being rewritten. In this context, business-as-usual assumptions no longer suffice.

At Venture Insights, we have developed four robust scenarios that explore how Australia’s media industry might evolve through to 2035. These scenarios are designed not as predictions, but as structured narratives to help industry leaders, investors, and policymakers understand the forces shaping the next era of media—and to plan for uncertainty with greater clarity.

Our models incorporate detailed forecasts across key sectors—including TV, radio, print, digital, outdoor, and emerging formats—alongside varying assumptions about technology adoption, regulatory change, and audience behaviour.

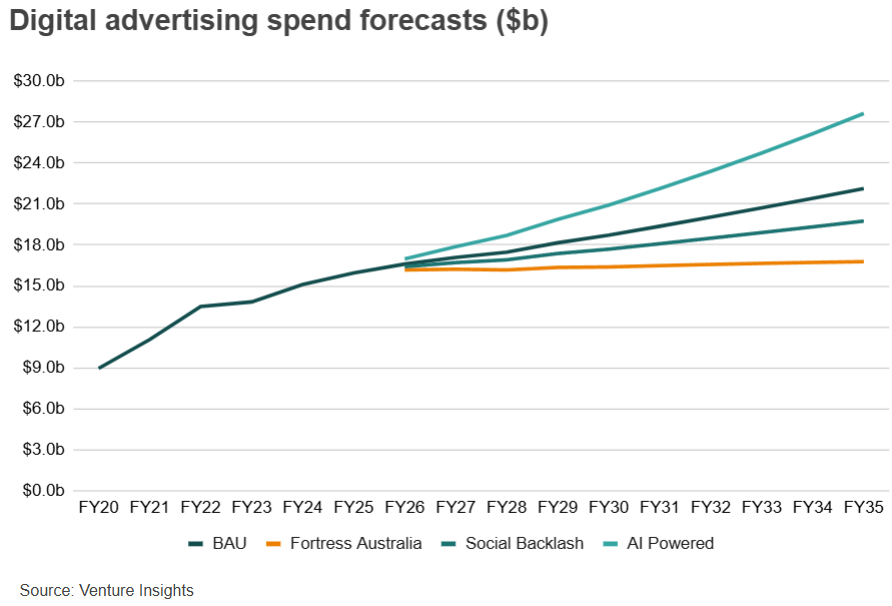

These scenarios build from a base case—a continuation of historical digital media growth trends with modest adjustments—and explore divergent pathways based on societal, technological, and regulatory dynamics. They pay particular attention to the evolving balance between local media and the global digital platforms who now generate around two-thirds of all advertising revenue. A summary view of how total digital advertising (search, display, and classifieds) would fare in these scenarios is presented below.

New scenarios for media markets

With this uncertainty in mind, we will explore four possible scenarios for the future of media markets in Australia. In coming reports, we will explore in more detail what could drive media in these directions, and how media industries and governments should respond.

Scenario 1: Business As Usual – Digital Dominance Continues

Overview: Digital continues to grow at a moderating pace, following established trends from the past decade.

Key Features:

- Continued shift of ad dollars from traditional to digital, but without exponential disruption.

- AI and platform dynamics grow steadily but coexist with legacy players.

- Incremental erosion of print and linear TV, with survivors consolidating around niches (e.g., specialist magazines, news radio, etc.).

- Outdoor and radio continue digital transitions, with podcasting and digital OOH (out-of-home) showing resilience and growth.

Implication: A steady evolution with winners and losers, but no dramatic breaks from the current trajectory.

In this scenario, the current stabilisation is merely a slowdown of existing trends, and the underlying trajectory persists. Digital platform advertising continues to take share from traditional media, albeit at a slower rate. Global tech platforms solidify their dominance, while local media players struggle to maintain relevance. No major policy interventions or consumer preference changes disrupt the existing market structure.

Scenario 2: Fortress Australia – Localism Fights Back

Overview: Australia introduces strict regulation and selective bans on foreign digital platforms to assert media sovereignty and protect local industries.

Key Features:

- Inspired by geopolitical distrust, misinformation concerns and backlash against tax avoidance strategies of global platforms.

- TikTok-style restrictions extended to some US-based platforms.

- Policies to prioritise local content, news production, and media employment.

- Potentially triggered by broader economic or strategic ruptures (e.g., US reneging on military or economic deals).

- Could involve state-backed platforms or regulatory frameworks mandating data localisation, editorial oversight, or platform accountability.

Implication: Radical restructuring of media landscape via policy—domestic platforms gain protected status.

In this scenario, the economic nationalist tendency is dominant. In response to global trade tensions and policy shifts, Australia and New Zealand implement measures to directly support local media such as newsroom subsidies and infrastructure support. Regulations cracking down on platform economic power favour domestic players, imposing restrictions or higher costs on global tech platforms. As a result, local media stabilises and regains some lost advertising share.

Scenario 3: Social Media Backlash – Consumers Turn Away

Overview: Australians disengage from social media and streaming services in reaction to misinformation, time-wasting content, and fatigue.

Key Features:

- Voluntary mass abandonment of platforms like Facebook, TikTok, and Netflix.

- Growing consumer desire for authenticity, verified content, and healthier digital habits.

- Shifts in advertising dollars as audiences fragment or withdraw.

- Rebirth of niche, specialist content with clear value propositions.

Implication: Digital growth slows significantly; traditional or alternative formats regain limited traction.

In this scenario, the social conservative tendency is dominant. Consumer trust in social media and digital advertising declines due to misinformation, data privacy concerns, and over-commercialisation. As engagement drops, advertisers shift budgets towards trusted, premium environments, including traditional media and emerging localised platforms. Social media search and display advertising revenue stagnates or even declines.

Scenario 4: AI-Powered Global Takeover

Overview: AI becomes the dominant force across all media formats, displacing traditional journalism, content production, and media employment.

Key Features:

- AI curates, produces, and delivers hyper-personalised content at scale.

- Traditional media roles (e.g., journalists, local radio hosts) are largely automated.

- Platforms like YouTube, with scalable, user-generated models, outcompete traditional broadcasters due to zero fixed content costs.

- News may be delivered by AI avatars tailored to users’ ideologies, preferences, and tone.

- Advertising follows AI-led content, accelerating the collapse of traditional channels.

Implication: The final “knockout blow” to legacy media; a complete restructuring of the media value chain.

In this scenario, the libertarian “tech bro” tendency is dominant. AI-driven content and advertising platforms dominate, creating highly personalised, automated media experiences. Global tech giants consolidate power, reducing reliance on human-created content and local media. The advertising industry becomes increasingly controlled by a few hyper-intelligent AI ecosystems.

Conclusion

For over a decade, Venture Insights has been at the forefront of tracking the evolution of the Australian advertising and media market. We have seen the digital disruption of print, the rise of subscription models, and the ongoing tensions between global tech giants and local media players. Our deep expertise in policy, regulation, and advertising market dynamics puts us in a unique position to forecast how these global shifts will shape Australia’s media industry.

Over the coming weeks, we will release a series of reports examining four critical scenarios that could define the future of Australian advertising:

- Digital Dominance Continues – Global platforms maintain their lead, squeezing local media further.

- Fortress Australia – Government intervention prioritises Australian-owned media over global tech.

- Social Media Backlash – Consumer trust erodes, reshaping ad spend and media influence.

- AI-Powered Global Takeover – AI rewires media and advertising, centralising power among a few global players.

Each report will provide granular forecasts, strategic insights, and clear implications for Australia’s biggest media and advertising players – including Nine, Seven West, News Corp, Google, Meta, ARN, SCA, and oOh!media.

This is not business as usual. The media landscape is shifting, and the choices made today will determine who thrives and who disappears. Venture Insights will be providing the data, insights, and strategic guidance to help businesses navigate the new reality.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.