BRIEF: Advertising Expenditure forecast: expect a rough FY24

- Publisher : Venture Insights

- Publish Date : June 29, 2023

Advertising Expenditure forecast: expect a rough FY24

TLDR version: This week we published our updated advertising expenditure (AdEx) forecast covering television, radio, digital, outdoor and cinema industries. Our headline expectation is that (after a flattish FY23) total AdEx in FY24 will fall by 5.0%. Another flattish FY25 will be followed by recovery.

This reflects a return to pre-pandemic normality. Changes in AdEx growth are closely correlated to changes in GDP growth, so advertising’s prospects are now tied to the future of the economy.

Advertising slowdown is well documented

The pandemic and associated disruption in FY20 only held the advertising industry back momentarily. The 7.2% fall in total advertising of FY20 was more than reversed with 14.8% growth in FY21. Growth in FY22 was 19.4%, although digital dominated this growth with a $2.6b increase.

But 1HFY23 ad revenue growth dropped to 4.0% YoY as higher interest rates increasingly weighed on confidence and spending. Added to this now is the growing risk of recession, both in Australia and globally.

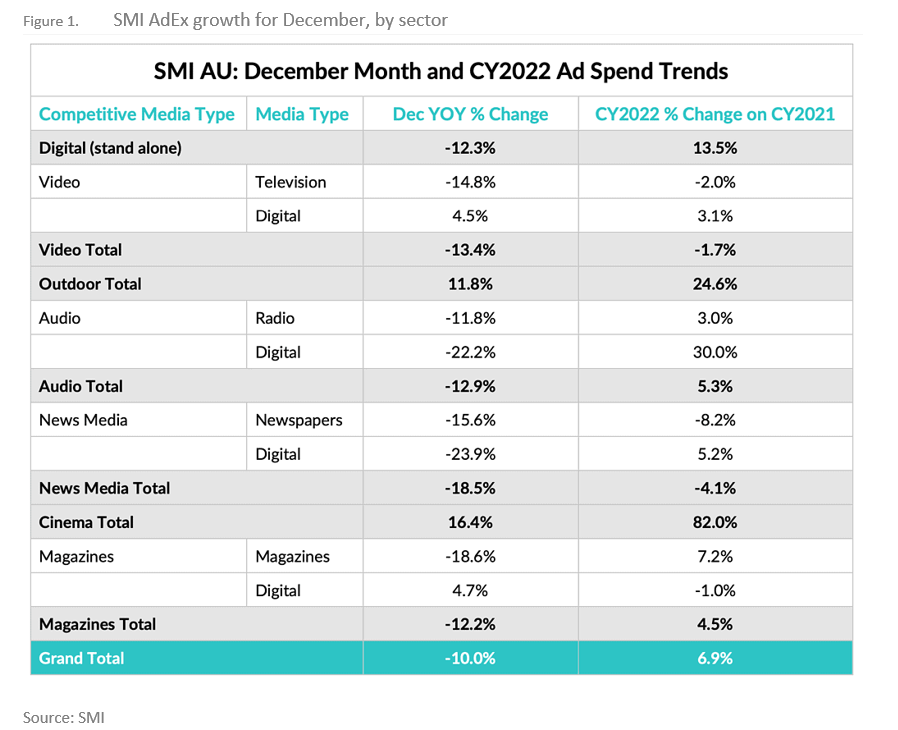

This has broadly been factored into the capital markets, so when SMI published data in February showing shrinking December ad budgets, most media stock prices moved only incrementally.

Looking to FY27, we expect outdoor advertising to be the fastest growing sector, followed by radio and digital. Despite radio’s current travails (it still hasn’t recovered its FY19 revenue), we think there is headroom for growth and that the industry’s online audio revenues will become material in the medium term. Digital growth is slowing, and we even expect a slight contraction in FY24. Digital currently accounts for 65.7% of all ad dollars, and we think this will rise by only another 2.0% by FY27. Cinema will take a hit in FY24 and will not recover FY22 revenue until FY27.

Television and print will experience revenue decline over FY22/27. The physical print industry is increasingly turning to subscription as physical ad revenues continue their decline, albeit at a slower rate. Broadcast television viewing is still declining, but the industry will make up some ground as BVOD viewing rises and as yields from programmatic ad placement improve.

Why does this matter?

Any contraction of advertising revenue is bad news, particularly for sectors like television and print that have declining audiences. However, some perspective is needed.

Despite the forecast FY24 decline, total ad spending will still be higher over the entire FY22/27 period than it was in pre-pandemic FY19. Despite a poor FY24, we expect a return to growth if the macroeconomic situation does not worsen. Admittedly, the risks are on the downside over the next few years, as recession fears (even in Australia) are growing. Much depends on whether the RBA can find a “narrow path” to a soft landing and the global economy holds up.

Further, ad-based industries are generally well-prepared for a contraction. Traditional industries like television, print and radio have done a lot of work in recent years to reduce their operational and capital cost base, and are therefore structurally well-placed to weather the challenge.

Slower growth in digital advertising (display, classifieds and search) may also see more discipline imposed on this sector as ad agencies seek more value.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.