BRIEF: Second “digital dividend” in UHF band still not certain

- Publisher : Venture Insights

- Publish Date : June 15, 2023

BRIEF: Second “digital dividend” in UHF band still not certain

Second “digital dividend” in UHF band still not certain

TLDR version: Better telco access to spectrum (and excessive spectrum pricing) was a theme of the CommsDay Policy Forum this week. Interest was expressed in gaining access to 600MHz UHF spectrum currently used by free-to-air (FTA) television. But the telco industry shouldn’t underestimate the difficulties of getting access to this spectrum. Full migration of FTA TV online is not likely because of Australia’s unique geography, while even a partial reallocation of TV spectrum faces some significant hurdles.

Telcos keen to acquire low band spectrum

A consistent theme of the CommsDay Policy Forum we attended on 14 June this week was the need for better allocation processes for spectrum, including a pricing process that better reflects the public value in expanding wireless access to telecommunications services. So far, so good.

But interest was also expressed in a second “digital dividend”, referring to the upgrade of TV compression technology and restacking of 600MHz UHF TV spectrum originally proposed in the Government’s 2020 Media Green Paper. The future of TV spectrum is now being examined by an industry/Government Working Group and no decision has yet been taken. But the amount of time already taken to review this issue makes it clear that this is no “lay down misere” for the telco industry.

Broadcast TV remains robust

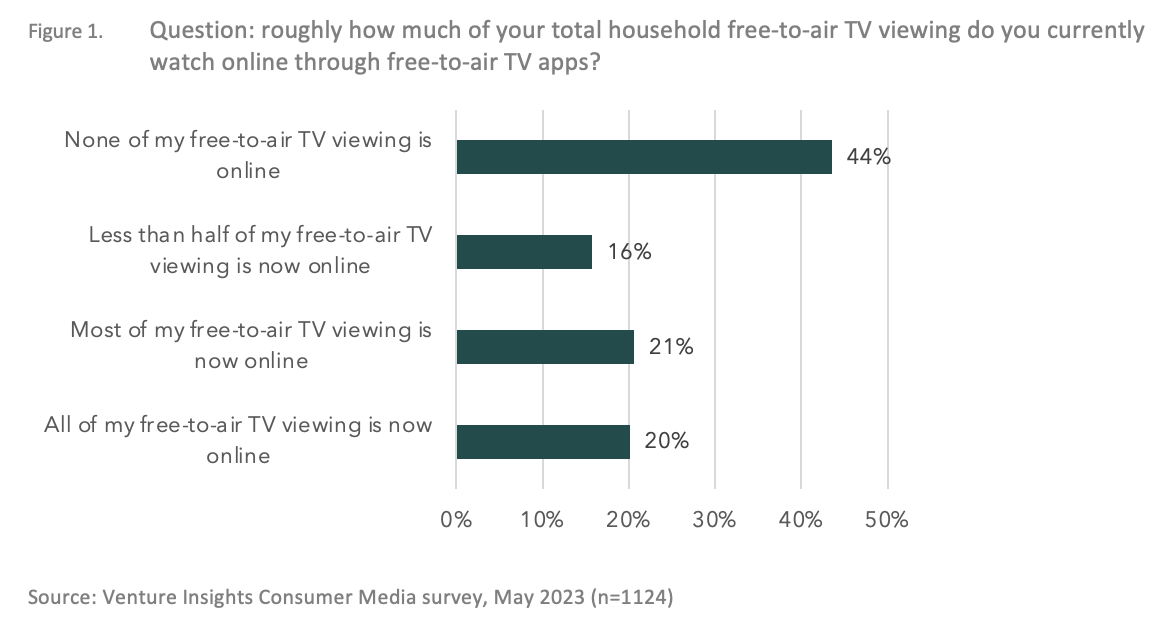

There are good reasons why the Government is examining the issue carefully. Our consumer media survey last month showed that 44% of households are still using broadcast for all of their FTA TV viewing. In contrast only 20% are using the Internet for all of their FTA TV viewing. One surprising result is that these numbers don’t vary significantly between urban and regional areas.

We estimate that around 10% of FTA TV viewing is currently taking place online. The reason that the share of fully online households is higher at 20% is that these households have much lower FTA viewing on average and watch more SVOD and AVOD services. FTA TV viewing minutes are dominated by “less online” households, including the 15% who have no fixed broadband at all.

The BBC’s steady migration away from terrestrial broadcasting was referenced at the Policy Forum as well. But we doubt that the UK example has much relevance to Australia with our much more dispersed populations and broadband availability issues. The US and Canada have reallocated much of their UHF TV spectrum, but those markets are much less dependent on UHF for TV than Australia is. Australia’s geography, dispersed population, and low pay TV penetration makes our situation unique.

Telcos with an appetite for TV spectrum will be encouraged to know that regional viewing is also migrating online. But there are warning signs there too. We noted a few weeks ago that remote TV service availability is a growing political issue for the Federal Government.

Why does this matter?

The original 2020 timetable for restacking of TV and reallocation of the unencumbered spectrum was ambitious, aiming for a decision before the end of 2022 and restacking in progress around 2025. This hasn’t happened, revealing that the original proposal failed to consider the realities of broadcast industry development. Restacking would restrict some significant FTA TV industry opportunities, particularly migration to 4K broadcasting, that would be a material cost for the TV industry.

It is possible that the TV industry might accept this cost if they conclude their real future is online, but that debate won’t be resolved quickly. The diversion of the original proposal into a Working Group discussion shows that the groundwork had not been done. What the Working Group will need to come up with is a roadmap for the FTA TV industry that sets out spectrum requirements for the long-term future and considers Australia’s unique geography and population distribution.

For the telecommunications industry, this means a long wait for 600MHz spectrum and ongoing uncertainty whether they will get any at all. It remains possible they will get the full 84MHz originally proposed, but that depends on the TV industry agreeing that an expansion of 4K broadcast is off the table. Failing that, a lower allocation would be the result, and possibly even a postponement of the digital dividend. In that case, the focus on higher frequencies for 5G network expansion would sharpen.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe, with a special focus on new disruptive technologies.

For more information go to ventureinsights.com.au or contact us at contact@ventureinsights.com.au.

Important notice: By accepting this research note, the recipient agrees to be bound by the following terms of use. This research note has been prepared by Venture Insights Pty Ltd and published solely for guidance and general informational purposes to authorised users under the terms of a licence agreement between Venture Insights Pty Ltd and its subscriber. You need to be expressly authorised to use it, and it may only be used for your internal business purposes and no part of this note may be reproduced or distributed in any manner including, but not limited to, via the internet, without the prior permission of Venture Insights Pty Ltd. If you have not received this note directly from Venture Insights Pty Ltd, your receipt is unauthorised. If so, or you have any doubt as to your authority to use it, please return this note to Venture Insights immediately.

This research note may contain the personal opinions of research analysts based on research undertaken. This note has no regard to any specific recipient, including but not limited to any specific investment objectives, and should not be relied on by any recipient for investment or any other purposes. Venture Insights Pty Ltd gives no undertaking to provide the recipient with access to any additional information or to update or keep current any information or opinions contained herein. The information and any opinions contained herein are based on sources believed to be reliable, but the information relied on has not been independently verified. Neither Venture Insights Pty Ltd nor its officers, employees and agents make any warranties or representations, express or implied, as to the accuracy or completeness of information and opinions contained herein and exclude all liability to the fullest extent permitted by law for any direct or indirect loss or damage or any other costs or expenses of any kind which may arise directly or indirectly out of the use of this note, including but not limited to anything caused by any viruses or any failures in computer transmission.

Any trade marks, copyright works, logos or devices used in this report are the property of their respective owners and are used for illustrative purposes only. Unless otherwise disclosed, Venture Insights has no affiliation or connection with any organisations mentioned in this report. However, the information contained in this report has been obtained from a variety of sources, including in some cases the organisations themselves. In addition, organisations mentioned in this report may be clients of Venture Insights.