BRIEF: NBN staff cuts won’t affect SAU pricing

- Publisher : Venture Insights

- Publish Date : March 20, 2023

NBN staff cuts won’t affect SAU pricing

TLDR version: NBN Co’s announcement that it is cutting around 10% of headcount shouldn’t have been unexpected. The shift from building the network to operating the network was always going to drive change in the company. But we don’t expect lower costs to drive any new concessions on wholesale pricing, because headcount reduction has undoubtedly been factored into NBN forward planning. In any case, the industry’s problems with NBN wholesale pricing don’t only arise from total cost, but include the existing CVC price construct.

NBN staff cuts will target management

The NBN Co CEO announced the staff cuts in an email to staff last week which emphasised the impact of growing competition on NBN Co’s business and the need for greater efficiency. Of NBN Co’s 4,650 headcount, roughly 500 will go (a reduction of over 10%).

The cuts will focus on general management, with field staff largely quarantined from the reductions. A spokesman was quoted in the AFR saying that the NBN Co “is seeking to preserve and grow field-based roles associated with its national fibre upgrade program, and the ongoing upgrades to its fixed wireless and satellite network”.

Why does this matter?

There were subsequent media reports that RSPs are now hoping that the cost reductions will flow through to lower pricing, especially as NBN Co faces more competition from alternative fibre, fixed wireless access, and LEO satellite. However, we doubt this will happen. While NBN Co is doubtless concerned about rising competition, it is unlikely that they will respond with major price cuts.

It is clear that NBN Co’s strategy is rather to upgrade and improve the network to increase its differentiation, while managing down the overhang of its accumulated losses ($30 billion and possibly more won’t be recovered).

And while LEO satellite and fixed wireless access do place competitive pressure on NBN Co, Chorus and other wholesale fibre providers in New Zealand have weathered a much bigger fixed wireless storm that NBN Co faces, and remain in the game because they can offer gigabit speeds to differentiate themselves. NBN Co is steadily positioning itself to do the same over most of its footprint by 2025, which is why field staff will not be cut and rollout and upgrades will continue.

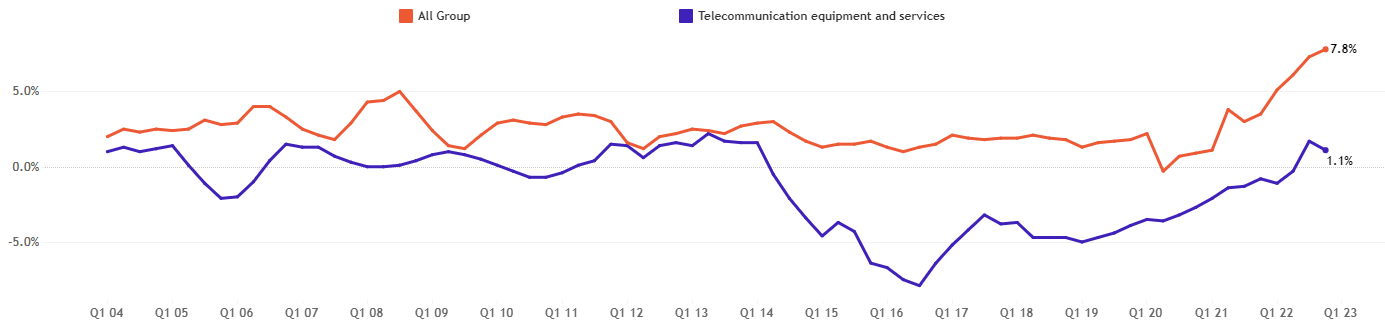

Part of the solution to Australia’s broadband pricing problem is to lift retail prices, not just to cut wholesale ones. In New Zealand, a wholesale price hike of 5.5% was recently approved and passed on to users with barely a whimper of protest. Meanwhile, CPI has been negative in the Australian telco industry for nearly a decade. Why?

Figure: Telecommunications services & equipment CPI vs Total CPI, 1984-2020

Source: ABS

One culprit is Australia’s volume-based CVC price, which does not exist in New Zealand where RSPs pay only a flat monthly fee for a connection. No-one likes price increases, but passing on a flat wholesale price increase isn’t hard to do when the culprit (Chorus) is ready to hand.

In Australia, it is very hard to market price hikes that are driven by capacity growth that is largely invisible to end users. This leaves RSPs to carry the burden of rising usage in the form of lower margins.

All this means that eliminating the CVC is much more important long-term than marginal changes in price levels. This will make it easier to drive some much-needed price inflation in the broadband market.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe, with a special focus on new disruptive technologies.

For more information go to www.ventureinsights.com.au or contact us at contact@ventureinsights.com.au