BRIEF: NBN connections decline shows rising competition

- Publisher : Venture Insights

- Publish Date : March 6, 2023

BRIEF: NBN connections decline shows rising competition

TLDR version: ACCC data shows that NBN Co’s TC-4 connections fell for the first time in the December quarter. The data also shows that the traditional “big four” retail providers – Telstra, Optus, Vocus and TPG – continue to lose NBN share. This reflects the growth of alternative broadband technologies and the rise of challenger retail brands.

NBN connections fall for first time

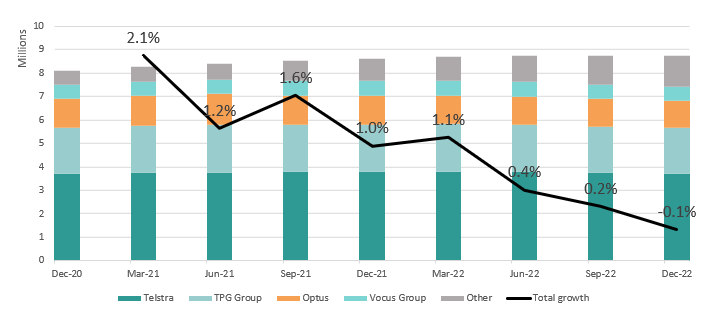

NBN Co’s reported TC-4 active connections fell for the first time in the ACCC’s latest quarterly NBN Wholesale Market Indicators Report. Total connections fell by about 9k (-0.1%) between September 2022 and December 2022. (NB: we estimate that around 8% of TC-4s are used for voice-only services, so the totals in the ACCC’s report are somewhat higher than total broadband connections in the market. They are nevertheless a good proxy for broadband growth).

To keep the decline in perspective, total TC-4 connections are still 8k higher than June 2022. But the quarterly growth rate of NBN active connections has been slowing steadily over the last few years, and it is possible that we will now see slow but steady declines for a while.

NBN TC-4 active connections by operator, and total quarterly growth rate

Source: ACCC, NBN Wholesale Market Indicators Report

Big four lose ground

The second major trend is the growth of the Others, including Southern Phone (AGL), Superloop and Aussie Broadband. “Other” connections have grown at 46.2% CAGR over the last two years, while the top 4 – Telstra, Optus, TPG and Vocus – have been collectively gone down -0.5%. Others now account for 8.0% of total TC-4 connections.

There are big variations amongst the “big four” though. Vocus is up 4% CAGR over the last two years, validating its claim that its retail business is on the mend and positioning it better for a future sale. Telstra and TPG were basically flat at 0.2% and -0.5% respectively, though we know that they have also been gaining non-NBN fixed wireless connections. Optus is down -4.6%. We don’t have much historical data for the “Others”, but Aussie Broadband now has 605k (almost as big as Vocus), Superloop 213k, and Southern Phone 102k active connections.

There are signs that LEO satellite is starting to make an impact in rural areas. NBN satellite connections peaked in December 2021 at 110k connections, but this has now fallen to 102k. Growth in NBN fixed wireless is consistent with earlier years, so they probably haven’t gone there. It’s more likely that these customers have found non-NBN alternatives.

Why does this matter?

These numbers add to the evidence that we’ve reached an inflexion point in both wholesale and retail broadband markets.

In the wholesale market, alternatives such as independent fibre and fixed wireless are now weighing on NBN household connection growth, increasing its reliance on the enterprise market. This means there will be continued pressure on the enterprise data & connectivity revenues of the other telcos as NBN Co seeks new customers in that segment.

In the retail market, the long period of consolidation we saw up to 2018 is very much over. The “Other” players are showing that it is possible to grow market share with good, targeted marketing and a focus on service. The question now is whether this growth is sustainable. Depressed share prices suggest there is still some scepticism of the ability of the Others to translate their successes into scale and margin organically. A future Vocus sale of Dodo may offer a new opportunity for consolidation and scale.